This is the question that stops most first-time buyers before they even start looking. They hear "20% down" from somewhere, do the math on a $400,000 house, land on $80,000, and quietly give up. So let's fix that right now.

The Short Version

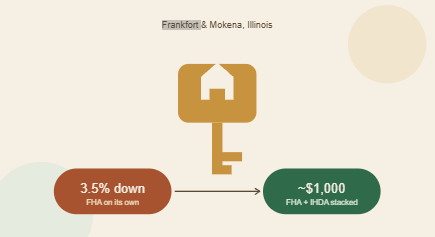

- FHA loan: 3.5% down with a 580+ credit score. On a $400,000 house, that's $14,000.

- Conventional (HomeReady/Home Possible): As low as 3% down if you qualify by income, generally needs a credit score around 620.

- VA loan: 0% down if you're an eligible veteran or service member.

- FHA + IHDA stacked together: Down payment assistance can cover most or all of that 3.5%, leaving you with as little as $1,000 out of pocket.

That last option is the one most Frankfort and Mokena buyers don't know exists until someone tells them.

How the FHA + IHDA Combo Actually Works

Illinois runs a state-backed down payment assistance program through IHDA, and it stacks directly on top of FHA financing. Here's what's available:

- Access Forgivable — 4% of purchase price, up to $6,000. Forgiven monthly over 10 years, so if you stay in the home, you never pay it back.

- Access Deferred — 5% of purchase price, up to $7,500. Interest-free, and you don't repay it until you sell, refinance, or pay off the mortgage.

- Access Repayable — 10% of purchase price, up to $10,000. Interest-free, repaid monthly over 10 years.

- Access Home — 6% of purchase price, up to $15,000. A deferred second mortgage with no monthly payment.

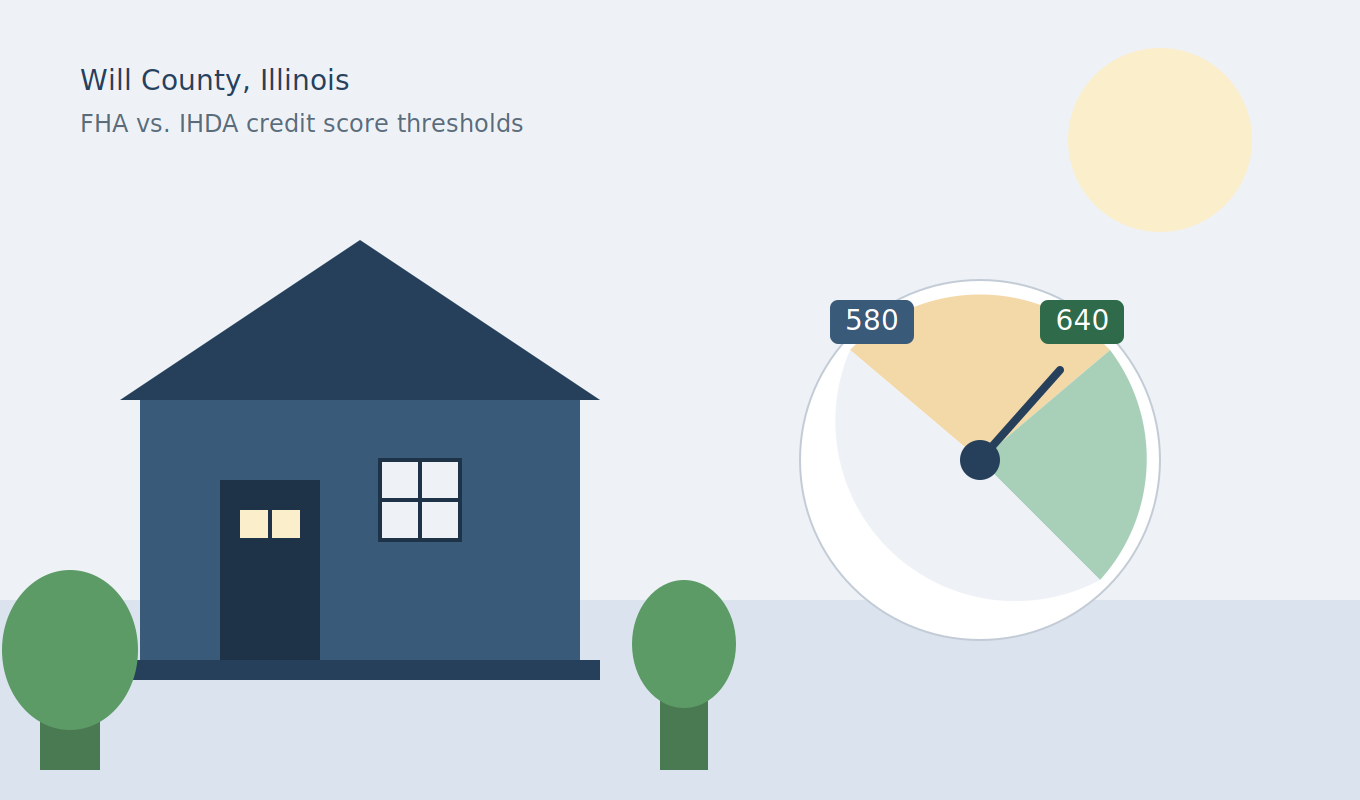

To use any of these, you need a 640 credit score — that's higher than FHA's own 580 minimum, which trips people up more than anything else in this process.

Once you're using IHDA assistance, your own out-of-pocket contribution is capped at $1,000 or 1% of the purchase price, whichever is greater. That's the number that makes people's jaws drop when I explain it on the phone.

What Determines Which Program Fits You

- Credit score under 640: FHA on its own is likely your path — still just 3.5% down.

- Credit score 640+: FHA or conventional, with IHDA assistance layered on to cover most of the down payment.

- Veteran or active-duty: VA loan, 0% down, no assistance program needed.

- Buying above $541,287: That's the 2026 FHA loan limit for Illinois, so a higher-priced home may need to go conventional instead.

Important Exception: What Most Articles Get Wrong

Here's something almost nobody writing about this topic mentions:

Frankfort isn't entirely in Will County. A small portion of the village actually sits across the line in Cook County.

Why does that matter for your down payment? IHDA's income limits and purchase price limits are set per county, and they're not identical between Will and Cook. Two homes a few blocks apart in Frankfort could technically fall under different limit tables depending on which side of that line they're on. If you're house-hunting in Frankfort specifically, that's worth confirming before you assume your numbers line up with a neighbor's.

Mokena doesn't have this issue — it sits entirely within Will County — but it's exactly the kind of detail a generic "down payment assistance in Illinois" article has no reason to know, and it can quietly change what you qualify for.

The Bottom Line

You don't need 20% down, and in most cases you don't need anywhere close to it. The real question isn't "how much do I need" — it's "which combination of programs gets me there with the least out of pocket," and that answer depends on your credit score, your county, and the price range you're shopping in.

As an IHDA-approved lender serving Will and Cook County, I can run your actual numbers — credit score, target price, which side of the Frankfort county line you're looking at — and tell you exactly what you'd need to bring to closing. Not a rough estimate. The real number.

This article reflects information as of July 2026. Terms and eligibility change — confirm current details with a licensed loan officer before making financial decisions.