Quick answer: In Will County, most first-time buyers need at least a 580 credit score to qualify for an FHA loan — but if you want Illinois' IHDA down payment assistance stacked on top, that number jumps to 640.

Written by Jimmy White, Mortgage Loan Officer, NMLS #1363362 — LeaderOne Financial, serving Will County homebuyers for over 11 years.

I get this question probably five times a week, usually from someone who's already talked themselves out of buying before they've even called me. So let's get the real numbers on the table.

The Short Version

- FHA loan: 580 credit score gets you 3.5% down. Below that, down to 500, you're looking at 10% down instead.

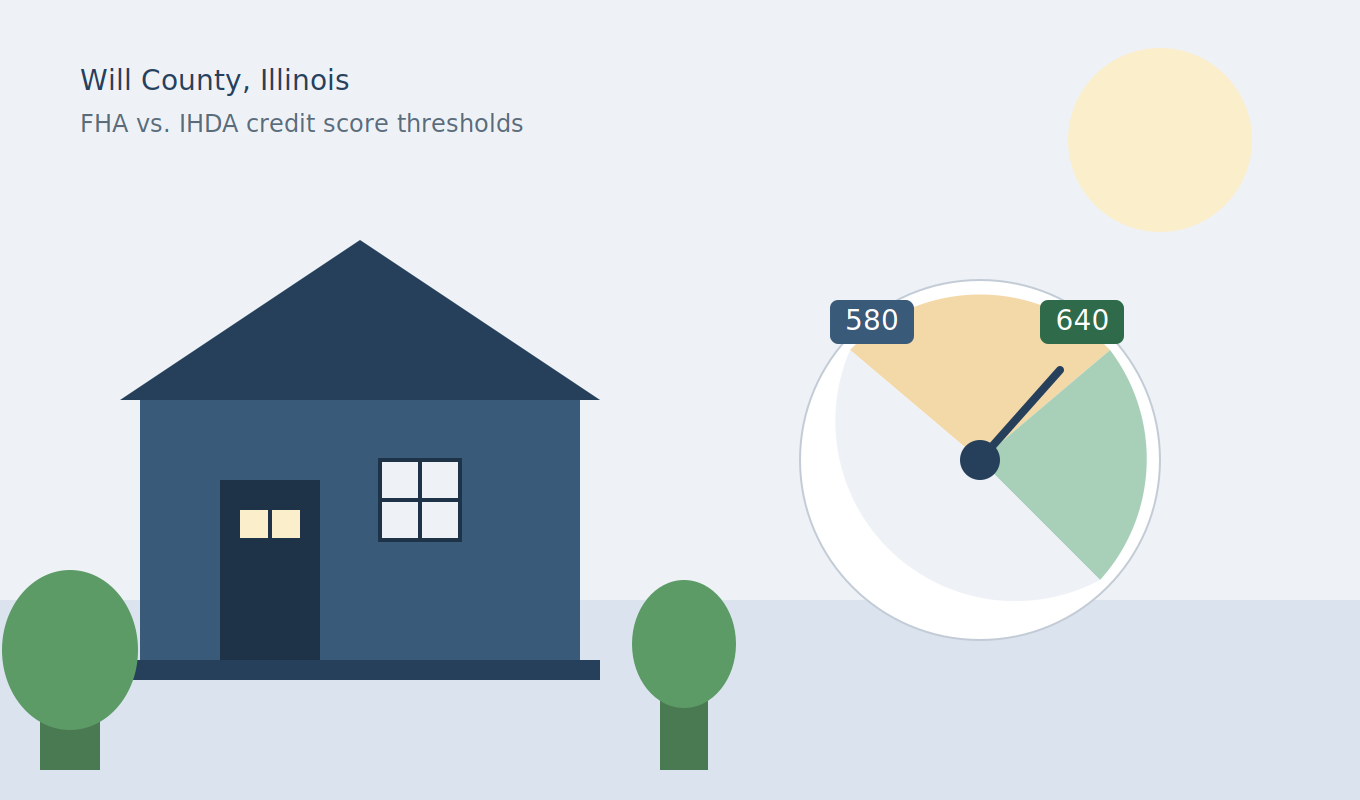

- IHDA down payment assistance: 640 credit score, no exceptions, regardless of what loan type you're using underneath it.

- Conventional loan: Typically 620 as a starting point, though this moves depending on the program and your lender's overlays.

That gap between 580 and 640 trips more people up than anything else in this business, and I'll explain why in a minute.

FHA: The National Floor

FHA sets the baseline for the whole industry, and HUD's own rules are pretty clear-cut:

- 580 or higher — you qualify for the standard 3.5% down payment.

- 500 to 579 — you're still eligible, but your down payment jumps to 10%.

- Below 500 — FHA financing isn't an option.

Here's the part nobody tells you: 580 is HUD's floor, not a guarantee from your lender. Individual lenders are allowed to set their own minimums on top of that — called overlays — and plenty of banks won't touch a file below 620 even though FHA technically allows it. So if someone quotes you "580" and then denies you, that's not FHA saying no. That's their own internal risk tolerance saying no. Different lenders, different answers.

Important Exception: What Most Articles Get Wrong

This is the one that matters most if you're buying in Will County specifically.

Almost every national blog post on this topic stops at "580 for FHA" and calls it a day. What they leave out:

Illinois' IHDA down payment assistance program requires a 640 credit score, regardless of loan type — FHA, conventional, VA, doesn't matter.

So if you're a Will County buyer with a 590 credit score, you can technically get an FHA loan. But you can't stack IHDA's down payment help on top of it until your score is at 640. That's a real gap, and it's the reason I ask about credit score in my very first conversation with any first-time buyer — because it changes which programs are even on the table.

IHDA also updates its income and purchase price limits for Will County every year, so the exact dollar cutoffs shift. I'd rather give you the current number over the phone than publish something here that's outdated in six months.

What If My Score Isn't There Yet?

You've got options, and none of them involve waiting around hoping your score fixes itself:

- Pull your credit with a lender, not a free app. Free credit apps often show inflated scores that don't match what mortgage underwriting actually uses.

- Pay down revolving balances before new accounts — utilization moves scores faster than almost anything else.

- Get a game plan, not a guess. A good loan officer can usually tell you what specific moves would get you from 590 to 640, and roughly how long it'll take.

The Bottom Line

Your credit score doesn't have to be perfect. It has to clear the right threshold for the right program — and in Will County, that threshold depends on whether you want IHDA's help or not.

As an IHDA-approved lender serving Will and Cook County, I can pull your credit, tell you exactly where you stand against both the FHA and IHDA thresholds, and lay out what it would take to close the gap if you're not there yet. No pressure, no sales pitch — just the real numbers for your situation.

This article reflects information as of July 2026. Terms and eligibility change — confirm current details with a licensed loan officer before making financial decisions.